India’s Digital Ocean Strategy:

Submarine Fiber Corridors, Bay of Bengal Geopolitics, and the Rise of the Global South Digital Network

By Saurabh Garg

Researcher | Market Observer | Astro-Strategic Analyst

EXECUTIVE SUMMARY

Submarine fiber-optic cables carry over 95% of global intercontinental internet traffic — yet they remain almost invisible to mainstream investment discourse. As artificial intelligence, hyperscale cloud computing, and digital sovereignty reshape geopolitics, control over undersea cable corridors is becoming a defining dimension of national power and commercial advantage. India, positioned at the convergence of the Bay of Bengal, the Indo-Pacific, and the Global South, now stands at an inflection point: transitioning from internet consumer to strategic digital transit civilization. This report examines the structural investment thesis, identifies key equity themes, and maps the emerging risk and opportunity landscape for institutional investors and research teams.

I. The Silent Infrastructure Beneath the World Economy

The internet, as most investors model it, is a collection of software platforms, cloud providers, and semiconductor manufacturers. What rarely enters equity models is the physical substrate that makes the entire digital economy possible — a global web of submarine optical fiber cables, most of them laid in the 1990s and 2000s, now carrying data volumes that their designers never anticipated.

The scale is staggering: as of 2024, more than 550 active submarine cable systems span approximately 1.4 million kilometres of ocean floor. They carry banking transactions, equity trades, AI model training data, cloud compute workloads, military communications, and streaming traffic — nearly all of it moving at the speed of light through strands of glass thinner than a human hair. [^1]

For stock market professionals, the relevance is direct: every order flow system, every algorithmic trading engine, every inter-exchange arbitrage strategy depends on latency characteristics that are fundamentally determined by these undersea routes. A submarine cable failure in the Red Sea or South China Sea is not an abstraction — it is a system-level risk event that can disrupt market connectivity across entire regions.

In January 2024, three submarine cable cuts near Yemen disrupted internet connectivity across East Africa, the Middle East, and parts of South Asia — demonstrating the cascading, cross-border impact of single-corridor dependencies. Recovery timelines extended to 8–12 weeks due to limited repair vessel availability.

II. The Geopolitical Compression: Why Routes Are Becoming Contested

The geopolitical context around submarine cables has changed fundamentally in the past five years. Three overlapping pressures are converging simultaneously.

A. The Chokepoint Problem

Nearly 40% of the world’s submarine cable traffic transits through a handful of maritime chokepoints — the Strait of Malacca, the Bab-el-Mandeb (Red Sea entry), and the South China Sea. Each of these corridors faces distinct and escalating geopolitical risk:

| Chokepoint | Risk Profile & Market Implication |

|---|---|

| Strait of Malacca | 150,000+ vessels annually. Any China–Taiwan escalation scenario disrupts major East–West cable routes serving $7+ trillion in daily global trade finance. |

| Red Sea / Bab-el-Mandeb | Houthi attacks (2024) triggered rerouting of 15% of global shipping. Cable infrastructure in the same corridor faced heightened sabotage risk. |

| South China Sea | Disputed territorial claims create ambiguity over cable maintenance rights. Chinese dredging activities in certain zones raise long-term infrastructure security concerns. |

| Taiwan Strait | Hosts some of Asia’s most critical cable landing stations. A blockade scenario would represent one of the largest single-corridor disruptions in digital history. [^2] |

B. The Sovereignty Dimension

Parallel to physical risk, a second structural shift is underway: digital sovereignty. Nations — particularly in the Global South — are reassessing overdependence on cable infrastructure owned, operated, or routinely accessed by a narrow set of hyperscale technology companies based in the United States.

The US TEAM telecom reviews, EU Digital Markets Act provisions, and India’s emerging data localization frameworks all point in the same direction: governments want trusted, domestically rooted digital corridors. This creates regulatory tailwinds for Indian infrastructure operators, as foreign-owned cable systems seeking India landing rights will increasingly need local consortium partners. [^3]

C. The AI Demand Shock

Perhaps the most underappreciated factor in submarine cable economics is the pace of AI-driven bandwidth demand. Training a single frontier AI model today requires moving petabytes of data between compute clusters, storage systems, and inference nodes distributed across continents. The IEA projects global data center power consumption will exceed 1,000 TWh annually by 2026 — implying a commensurate surge in intercontinental data transfer requirements. [^4]

Existing cable systems — many designed for 2000s-era traffic assumptions — are increasingly capacity-constrained on key routes. New cable deployments are not merely telecom infrastructure projects; they are AI-era critical infrastructure. Investors who model this as a simple telecom capex cycle are misreading the demand structure. [^5]

III. India’s Strategic Positioning — The Structural Investment Thesis

India’s positioning in this landscape is not accidental. It reflects a convergence of geography, policy, and corporate strategy that is beginning to create measurable investment-grade opportunity.

A. Geographic Asymmetry

India sits at the natural centre of the Indo-Pacific digital corridor — geographically equidistant between East African cable landing points, Gulf data centre hubs, Southeast Asian exchange nodes, and European terminus stations. No other single country commands comparable geographic optionality across all four of these corridors simultaneously.

The Bay of Bengal specifically is transitioning from a secondary corridor to a primary one — driven by the expansion of Southeast Asian digital economies, Bangladesh’s rapid internet penetration growth, and India’s own AI infrastructure build-out along its eastern seaboard. [^6]

B. The TRAI Policy Signal

India’s Telecom Regulatory Authority (TRAI) issued a public consultation paper on submarine cable landing policy in early 2025 — a document that has received insufficient attention in financial markets. TRAI Chairman AK Lahoti explicitly framed submarine cable infrastructure as a national strategic priority in the AI era, not merely a telecom licensing matter.

Reading between the regulatory lines, this signals several things with investment relevance: accelerated permitting timelines for new cable landing stations, potential for government co-investment in strategic cable routes, and a preference for consortiums with meaningful Indian equity participation — all of which structurally advantage established Indian telecom and infrastructure operators over purely foreign-owned entities. [^7]

C. The Corporate Build-Out — Beyond the Headlines

Reliance Jio: First-Mover at Scale

Jio’s dual-system submarine strategy — the India-Asia-Xpress (IAX) connecting Mumbai and Chennai to Singapore via Thailand and Malaysia, and the India-Europe-Xpress (IEX) routing through the Middle East and North Africa — represents the most ambitious India-centric cable programme in the nation’s history. Together, these systems are designed to position Jio as both a domestic internet backbone provider and an international transit operator, capturing margin at both ends of the data flow. [^8]

Bharti Airtel: The Enterprise Connectivity Moat

Airtel’s international business division operates existing subsea cable capacity through its partnership networks and is expanding enterprise connectivity across Africa and ASEAN markets. As multinational corporations deepen India operations — driven by both market opportunity and China+1 supply chain diversification — Airtel’s enterprise connectivity stack positions it to capture business-grade traffic growth. [^9]

Tata Communications: The Incumbent Advantage

Tata Communications holds one of the most substantial existing global subsea cable footprints of any Indian entity — built over decades through the Tata group’s international telecom investments. Its data products business, which serves enterprise and financial services clients globally, is structurally positioned to grow as Indian-origin data traffic volumes expand.

The key distinction for research teams is between direct cable operators (Jio, Airtel, Tata Communications) and ecosystem enablers (cable manufacturers, data centre operators, power infrastructure providers). Risk-return profiles differ significantly. Direct operators face substantial capital commitments and consortium execution risk; ecosystem enablers participate in the same demand wave with lower capital intensity and often more predictable revenue profiles.

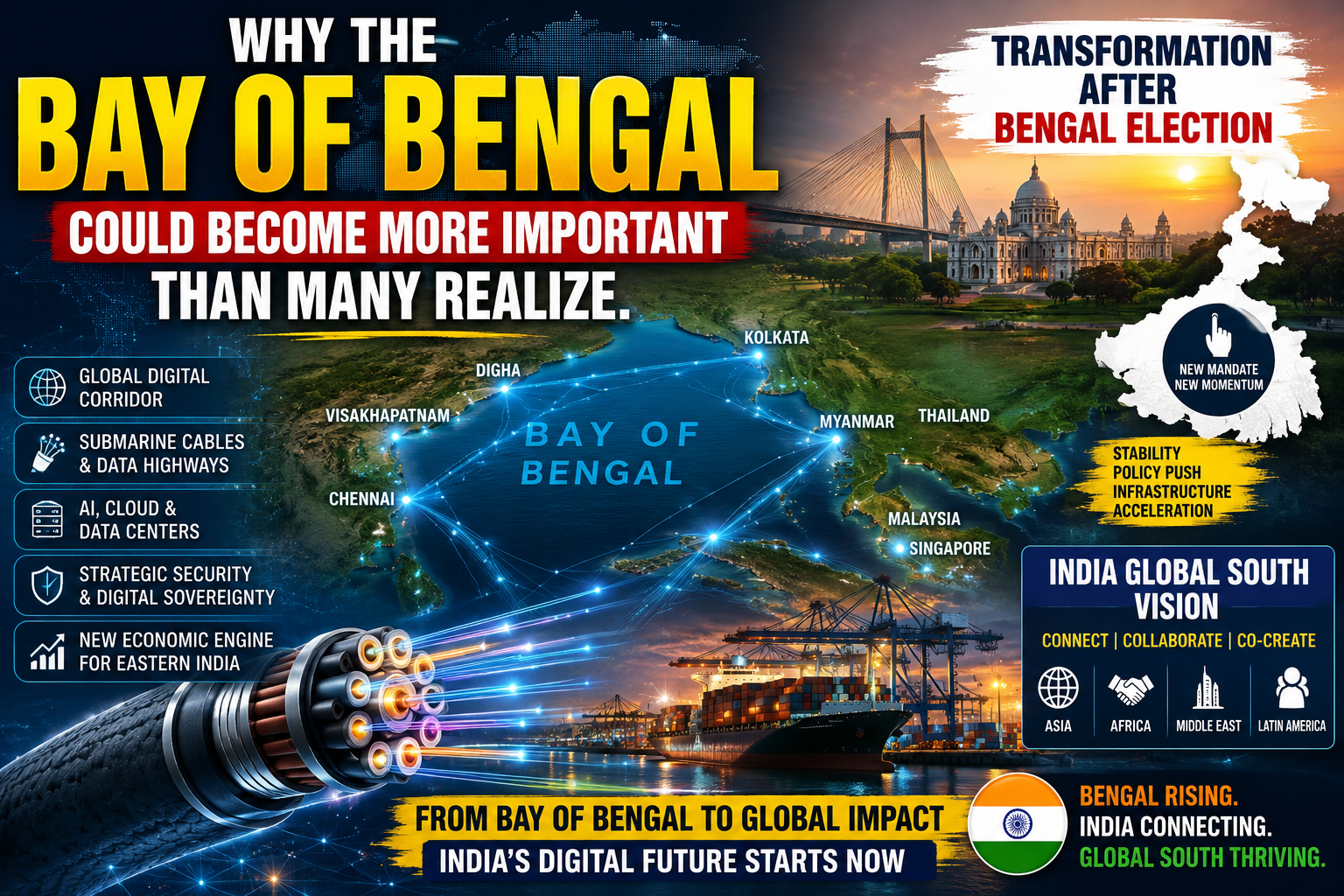

IV. The Bay of Bengal — Anatomy of an Emerging Digital Corridor

The Bay of Bengal is not currently the dominant submarine cable corridor — that distinction belongs to the trans-Pacific and trans-Atlantic routes. But the forward-looking case is compelling, and the directional shift is already visible in project announcements and policy postures.

A. Why the Eastern Seaboard Matters Now

India’s western coastline — anchored by Mumbai and Chennai — has historically dominated submarine cable landings. But the emerging Bay of Bengal story is about the eastern coastline: Visakhapatnam, the Odisha coast, and ultimately the Andaman and Nicobar Islands, which occupy a position of extraordinary strategic value in any future Indo-Pacific digital architecture.

| Eastern Coastal Asset | Strategic Digital Relevance |

|---|---|

| Chennai (already active) | Existing multiple cable landings; likely to anchor Bay of Bengal gateway expansion. |

| Visakhapatnam | Navy base adjacency + port infrastructure; candidates for dual-use (commercial + defense digital) cable landing. |

| Odisha Coast / Digha region | Underdeveloped cable infrastructure; greenfield opportunity for new landing station development. |

| Andaman & Nicobar Islands | Strategically positioned between Bay of Bengal and Malacca Strait; potential future node for India–ASEAN cable routing. |

B. The ASEAN Integration Dimension

Vietnam, Indonesia, and the Philippines are each undergoing rapid digital infrastructure expansion, driven by a combination of domestic consumption growth and manufacturing FDI relocation away from China. Their bandwidth demands — both for domestic internet and for cross-border enterprise connectivity — will require substantially expanded submarine cable capacity into and through the Bay of Bengal corridor. India’s ability to position itself as a preferred transit and landing partner for ASEAN-origin cable systems depends on regulatory certainty, expedited permitting, and competitive pricing for cable landing station services — all of which the TRAI consultation paper is attempting to address. [^10]

C. The Africa Vector

Africa represents arguably the most underappreciated demand driver in global submarine cable economics. The continent’s internet penetration rate remains below 40% as of 2024, but urban digital adoption is accelerating rapidly — and new cable systems designed to serve African coastal nations are increasingly routing through Indian Ocean pathways that intersect with India’s western and eastern coasts. Airtel Africa’s network footprint creates a natural commercial rationale for India-to-Africa cable route investment, while the Global South geopolitical framing provides a diplomatic overlay that could support state-backed financing structures. [^11]

V. The Data Centre Nexus — Where Cable Meets Cloud

Submarine cables are infrastructure inputs; data centres are the consumption endpoints. The investment thesis connecting the two is straightforward: cable capacity expansion without corresponding data centre build-out creates bottlenecks, and vice versa. India is building both simultaneously — and that simultaneity is what makes the current moment structurally different from prior infrastructure cycles.

Mordor Intelligence estimates India’s data centre market will grow from approximately $7.2 billion in 2024 to over $20 billion by 2029, driven by hyperscaler investments (AWS, Microsoft Azure, Google Cloud all have announced major India expansions) and domestic cloud adoption. Each hyperscaler’s India presence increases the volume of cross-border data traffic that needs to transit through submarine cables — creating a self-reinforcing demand cycle. [^12]

For research teams mapping the supply chain: power infrastructure is the binding constraint. A hyperscale data centre requires 100–500 MW of reliable power. In a country where grid reliability remains uneven, companies with credible power delivery capability — whether through grid connectivity, captive renewable generation, or battery storage systems — hold genuine competitive advantage in capturing data centre capex. [^13]

Each 1% increase in India’s data centre capacity absorption is estimated to generate approximately 2.5–3x multiplier demand for inland fiber connectivity, power grid upgrades, and cooling infrastructure — making telecom cable manufacturers and power systems integrators indirect but meaningful beneficiaries of the hyperscaler investment wave.

VI. Risk Framework — What Can Go Wrong

| Risk Category | Assessment |

|---|---|

| Geopolitical Escalation | A rapid China–Taiwan military scenario could disrupt trans-Pacific cable routes and trigger emergency rerouting demands — temporarily beneficial for India corridor operators but with systemic market volatility implications. |

| Regulatory Delays | India’s cable landing permitting process has historically been slow. TRAI consultation signalling is constructive, but execution risk remains. Coastal clearances, defence NOC requirements, and environmental permissions add timeline uncertainty. |

| Consortium Execution | Major submarine cables are consortium projects involving multiple international telecom operators. Jio and Airtel’s ability to attract and retain consortium partners at favourable commercial terms is an ongoing execution variable. |

| Technology Disruption | Low Earth Orbit (LEO) satellite constellations (Starlink, OneWeb) could partially substitute for submarine cables in remote or thin-route markets, though latency and capacity constraints make them unlikely to threaten high-volume trunk routes in the medium term. |

| Capital Cycle Risk | Infrastructure investment cycles are long and lumpy. A global recession or significant rise in debt financing costs could delay cable deployment timelines, creating overhang on capital-intensive operators. |

| Currency & Regulatory Arbitrage | International cable consortium revenues are typically USD-denominated, creating INR/USD currency exposure for Indian operators. Regulatory changes in partner country markets (Singapore, Malaysia, UAE) can affect landing rights and transit pricing. |

VII. Strategic Equity Watchlist — Thematic Mapping

The following tables map publicly listed Indian companies across the submarine cable and digital infrastructure value chain. These are presented as a thematic research framework, not as investment recommendations. Investors should conduct independent due diligence on each name, including analysis of valuation, balance sheet quality, and sector-specific regulatory exposure.

Large Cap — Direct & Structural Exposure

| Ticker | Company | Investment Relevance for This Theme |

|---|---|---|

| RELIANCE | Reliance Industries / Jio | Most direct submarine cable exposure via IAX & IEX systems. Integrated data centre + cloud + AI infra strategy. |

| BHARTIARTL | Bharti Airtel | International enterprise connectivity, Africa + ASEAN digital expansion, existing subsea footprint. |

| TATACOMM | Tata Communications | India’s deepest existing global submarine cable and data products network. |

| ADANIENT | Adani Enterprises | Smart ports, AdaniConneX data centres, coastal industrial cluster development. |

| LT | Larsen & Toubro | Marine infrastructure EPC, data centre construction, industrial digital projects. |

| POWERGRID | Power Grid Corp | National fiber backbone via power transmission corridor; AI-era grid relevance. |

| RAILTEL | RailTel Corporation | Strategic inland fiber backbone through rail network — last-mile to coastal landing stations. |

| BEL | Bharat Electronics | Defence-grade secure communications; strategic digital integration with Navy coastal assets. |

Mid Cap — Ecosystem Enablers

| Ticker | Company | Investment Relevance |

|---|---|---|

| HFCL | HFCL Ltd | Optical fiber & cable manufacturing. One of the most direct domestic supply chain beneficiaries. |

| TEJASNET | Tejas Networks | Optical networking equipment for submarine cable terrestrial segments. |

| POLYCAB | Polycab India | Fiber + power cable manufacturing; data centre electrification demand. |

| KEI | KEI Industries | Telecom and industrial cable manufacturing; infra electrification demand. |

| RRKABEL | RR Kabel | Cable infrastructure expansion across telecom and industrial segments. |

| NETWEB | Netweb Technologies | AI servers and HPC systems; demand driven by data centre build-out. |

| CGPOWER | CG Power | Power systems and transformers for data centre and grid infrastructure. |

| PERSISTENT | Persistent Systems | AI/cloud engineering services; software layer of digital infrastructure. |

| ITI | ITI Limited | Telecom manufacturing; strategic government digital project exposure. |

Small Cap — Niche & Emerging Optionality

| Ticker | Company | Investment Relevance |

|---|---|---|

| VINDHYATEL | Vindhya Telelinks | Optical fiber cable manufacturing; direct demand from cable expansion. |

| AKSHOPTFBR | Aksh Optifibre | Optical fiber and telecom networking niche play. |

| DATAPATTNS | Data Patterns | Defense-grade communication electronics; secure systems for Navy coastal infra. |

| HCLTECH | HCL Technologies | Cloud infra modernisation and enterprise network services. |

| BONDADA | Bondada Engineering | Telecom infrastructure rollout and tower services. |

| MOSCHIP | MosChip Technologies | Semiconductor and embedded design; AI-era chip design optionality. |

Port & Coastal Infrastructure

| Ticker | Company | Strategic Link |

|---|---|---|

| ADANIPORTS | Adani Ports & SEZ | Smart port + digital logistics corridor integration; cable landing adjacency. |

| JSWINFRA | JSW Infrastructure | Maritime infrastructure expansion along Indian coastline. |

| COCHINSHIP | Cochin Shipyard | Marine engineering for cable ship maintenance and repair. |

| SEAMECLTD | Seamec Ltd | Marine support vessel services; cable laying and repair ecosystem. |

VIII. The Long View — Civilizational Infrastructure

This report has deliberately stayed close to near-term market structure and investable equity themes. But it would be incomplete without acknowledging the longer arc of what is actually being built.

The twentieth century’s great infrastructure competitions were fought over oil pipelines, shipping lanes, and military basing rights. The twenty-first century’s version of that competition is being fought, quietly and largely invisibly, beneath the world’s oceans. The nations — and the corporations operating within them — that control trusted digital pathways will shape the terms of AI-era economic integration, financial market connectivity, and strategic communication for decades.

India’s emergence as a potential digital transit civilization is not inevitable — it requires sustained policy commitment, regulatory reform, and capital deployment over a multi-year horizon. But the directional indicators are more aligned than they have been at any previous point. For investors with a five-to-ten-year horizon, the structural tailwinds from AI infrastructure demand, Global South digital connectivity growth, and geopolitically driven route diversification all point in the same direction. [^14]

The most durable way to gain exposure to this theme is not through any single operator but through a basket approach spanning the cable ecosystem value chain: combine direct telecom operators (Jio, Airtel, Tata Comms) for core exposure, optical fiber manufacturers (HFCL, Vindhya Telelinks) for supply chain leverage, power infrastructure companies (CG Power, Polycab) for the data centre electrification overlay, and port operators (Adani Ports) for coastal infrastructure optionality.

IX. Conclusion

Submarine fiber-optic cables are among the most consequential and least understood assets in the global economy. For the Indian equity research community, the current moment represents a relatively early window to develop frameworks around a theme that will become increasingly mainstream as AI infrastructure investment scales, geopolitical route diversification accelerates, and India’s regulatory environment matures.

The Bay of Bengal digital corridor is not a single project or a single company — it is a structural transformation of how the world’s data moves across continents. Investors who map this transformation early, understand the ecosystem dependencies, and manage the execution risks accordingly, are positioning themselves at the leading edge of one of the defining infrastructure investment themes of the coming decade.

The future competition among nations will not be fought through territory alone. It will be decided, in significant measure, through control of the invisible highways of data flowing beneath the oceans — and India is now, more seriously than at any previous point in its history, building to compete.

References

[1] TeleGeography (2024). Submarine Cable Almanac 2024. Washington DC.

[2] TRAI (2025). Consultation Paper on Submarine Cable Landing Policy. New Delhi.

[3] UNCTAD (2023). Review of Maritime Transport. Geneva: United Nations.

[4] Council on Foreign Relations (2024). The Geopolitics of Subsea Cables. CFR Special Report.

[5] Jio Platforms Ltd. (2023). Annual Report. Mumbai: Reliance Industries.

[6] BIMCO & ICS (2024). Seafarer Workforce Report. Maritime security assessments.

[7] International Energy Agency (2024). Data Centres and Data Transmission Networks. Paris: IEA.

[8] McKinsey Global Institute (2023). Generative AI and the Economy. McKinsey & Company.

[9] Ministry of Electronics and IT (MeitY, 2024). National Data Center Policy Draft. New Delhi.

[10] Mordor Intelligence (2024). India Data Center Market Report 2024–2029. Hyderabad.

[11] Asia Times (April 2026). Silicon and Steel: Contest for the Bay of Bengal.

[12] Global Commission on the Stability of Cyberspace (2023). Norms for Submarine Cable Protection.

[13] Synergy Research Group (2024). Global Cloud Infrastructure Quarterly Report, Q4 2024.

[14] Bharti Airtel Ltd. (2024). Integrated Annual Report 2023–24. New Delhi.

[15] NASSCOM (2024). India Technology Industry Report 2024. New Delhi.

This report is produced for informational and research purposes only and does not constitute investment advice, a solicitation to buy or sell securities, or a recommendation of any specific financial product. The thematic watchlists included herein are frameworks for analytical research, not investment recommendations. All data cited reflects information available as of publication date and may be subject to change. Investors should conduct independent due diligence and consult qualified financial advisors before making investment decisions. Past performance does not guarantee future results.

")